Introduction

Logistics Industry Statistics: The logistics industry is experiencing transformative change on many fronts, marked by robust growth, innovation, and strategic adaptation to global, technological, and consumer pressures. Below is an independent market research-style outlook, examining each critical aspect with precise focus and simple language.

Advancements in automation, artificial intelligence (AI), and the Internet of Things (IoT) are rewriting the playbook for logistics. More companies now deploy warehouse robots for tasks such as sorting, picking, and packing, resulting in faster processes and fewer errors. AI-powered platforms, including route-planning tools, save fuel, shorten delivery times, and offer smarter responses to sudden disruptions. For example, Uber Freight used AI to cut “empty miles” by as much as 15%, directly improving efficiency and lowering operation costs.

Editor’s Choice

- Logistics costs can account for up to 30% of total delivery costs, making it a critical area for efficiency improvements and cost control across the supply chain.

- Transportation remains the largest cost driver, contributing 58% of total logistics expenses, followed by warehousing at 23%, inventory carrying at 11%, and administrative functions at 8%.

- Globally, 60–70% of logistics costs are attributed to transportation alone, highlighting the sector’s vulnerability to fuel price volatility and route inefficiencies.

- Delivery delays (46%) and fuel costs (39%) are identified as the top challenges that transportation carriers aim to address through digital and automation technologies.

- The supply chain sector accounts for approximately 8–10% of global GDP, underscoring its central role in economic performance and international trade facilitation.

- The global e-commerce logistics market is expected to reach USD 1.85 trillion by 2026, driven by rapid digital retail growth, consumer expectations for faster delivery, and last-mile innovations.

- Currently, 68% of global goods are moved via sea transport, reinforcing the critical importance of port infrastructure and maritime logistics in global trade flows.

- The average cost of logistics as a share of total sales stands at 13%, reflecting both operational complexity and opportunity for efficiency gains through optimization technologies.

- Nearly 85% of logistics businesses report operating at near full capacity, putting additional pressure on infrastructure, workforce availability, and technology adoption.

- Over 65 million people are employed across the global logistics industry, making it a key employment sector with growing demand for digital skills and automation expertise.

- The freight transportation sector contributes approximately 8% of total global greenhouse gas emissions, intensifying the need for cleaner energy solutions and modal shift strategies.

- Warehouse automation is shown to improve operational efficiency by up to 30%, while IoT deployments in logistics can deliver efficiency gains of up to 25%, particularly in real-time tracking and predictive maintenance.

- Blockchain is projected to save the logistics industry nearly USD 2 billion annually by 2025, mainly by reducing fraud, eliminating paperwork, and improving supply chain transparency.

- Average global parcel delivery times have improved by 30% since 2018, thanks to route optimization, automation, and better demand forecasting.

- Autonomous trucks could account for up to 35% of freight transportation in North America by 2030, presenting a major shift in labor demand and cost structure.

- Cold chain logistics now constitutes about 12% of the global logistics market, driven by increasing demand for temperature-sensitive goods like pharmaceuticals and fresh food.

- Electric trucks are forecasted to make up 30% of new freight vehicle sales by 2030, aligning with decarbonization goals and sustainable logistics initiatives.

- The global third-party logistics (3PL) market is anticipated to grow at a CAGR of 8.6% between 2022 and 2030, as outsourcing becomes a strategic lever for flexibility and scale.

Suggested Reading – Dropshipping Statistics, Facts and Trends

Financial Insights

Global Logistics and Trade

Trade Agreements: The UK-India free trade agreement (May 6, 2025) eliminates tariffs on 99% of Indian exports, benefiting textiles, engineering goods, IT, and financial services.

Regional Market Dynamics

- Asia-Pacific led the global logistics market in 2024, holding a 44.6% share. Growth was driven by the adoption of advanced logistics technologies and government policies promoting trade.

- Europe ranked second in 2024, but its expansion pace has been slower compared to other regions.

- North America held a 22% share in 2024 but is forecasted to overtake Asia-Pacific and Europe from 2025–2034, propelled by:

- Rapid growth in e-commerce

- Rising demand for same-day delivery

- Heavy investment in last-mile logistics and high-efficiency warehousing

Transport Modes:

- Water Transport was the fastest-growing in 2023, valued for cost efficiency and high cargo capacity. The market is projected to hit USD 983 billion by 2032, CAGR 6.2%.

- Rail Logistics is also expanding, with a CAGR of 4.1%, expected to reach USD 507 billion by 2034 from USD 355 billion in 2025.

(credit – infosys)

Sustainable Finance

The logistics sector is facing a critical turning point as its contribution to global carbon emissions could soar to 40% by 2050 if effective measures are not implemented, according to the European Environment Agency. This projection highlights the urgent need for sustainable logistics practices to mitigate climate impact. In line with the Paris Agreement, companies are now tasked with reducing their carbon emissions by 55% by 2030 compared to 1990 levels, a target that is driving major shifts in transportation and warehousing operations.

Europe alone has recognized the scale of this challenge, planning an additional annual investment of $663 billion between 2020 and 2030 to bolster its transport and storage sector’s climate goals, with the understanding that these upfront costs are far outweighed by the long-term benefits of climate action. The green logistics market is expanding rapidly, with a global valuation around $1.6 trillion in 2025, expected to more than double by 2034. This growth is fueled by regulatory pressures, technological advances, and shifting consumer preferences.

Companies are increasingly adopting strategies such as route optimization, electric and hydrogen vehicles, sustainable packaging, efficient inventory management, and reverse logistics to reduce emissions. The European Union’s tightening regulations, such as the expanded Emissions Trading System requiring shipping companies to account for 70% of their greenhouse emissions starting in 2025, are further accelerating the transition to greener operations.

Consumer behavior is an essential driver in this transformation. Studies reveal that 57% of consumers show strong interest in sustainable home delivery options, and 99% are willing to take extra steps to lessen their environmental footprint. However, a notable challenge remains as many consumers hesitate to pay extra for green delivery options. Despite this, sustainable practices present a key opportunity for logistics companies to connect with eco-conscious customers who value environmental responsibility.

The market outlook suggests that logistics players who embed sustainability deeply into their operations will not only comply with regulations but also gain competitive advantage by appealing to the growing environmentally aware consumer base. This alignment of economic and environmental interests signals a promising, though demanding, future for logistics companies as they strive to meet ambitious carbon reduction goals while maintaining service quality and cost-effectiveness.

(reference: infosys.com)

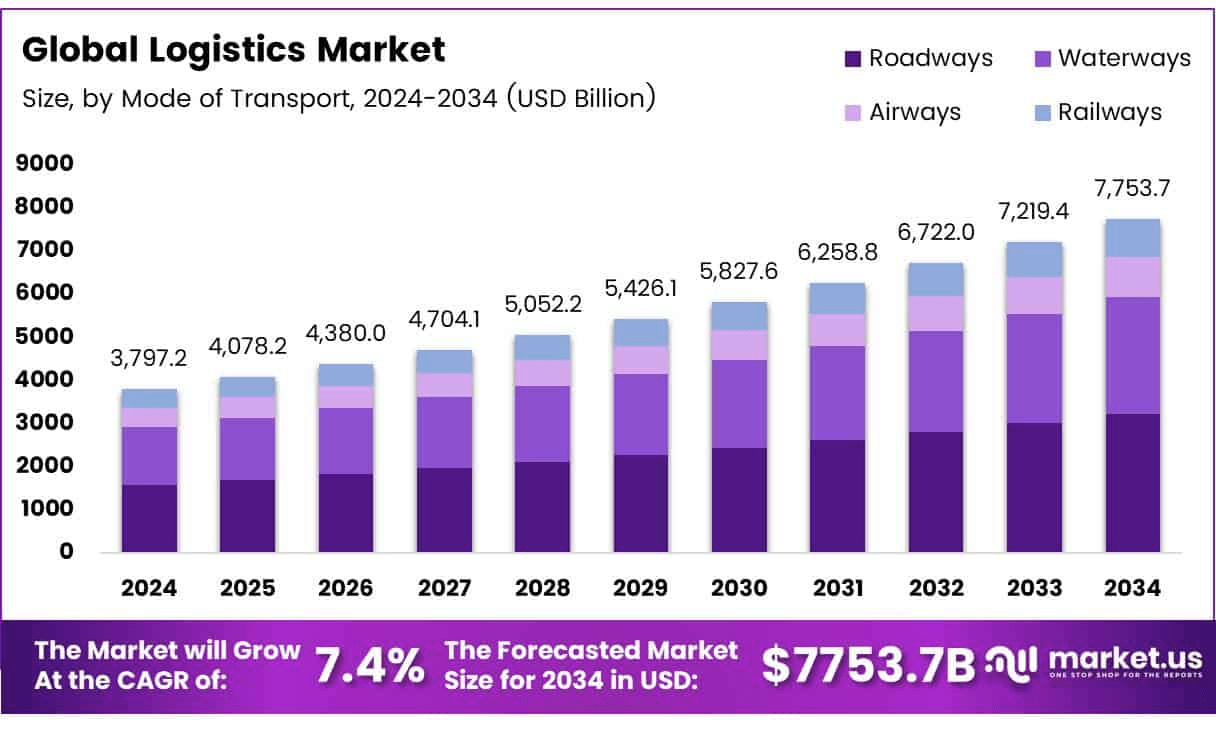

Logistics Industry Market Size

- The Global Logistics Market is projected to grow from USD 3,797.2 billion in 2024 to USD 7,753.7 billion by 2034, registering a CAGR of 7.4%.

- Road transport led the mode of transport segment with a 43.6% share in 2024, supported by its direct shipment capability and extensive geographical coverage.

- Transportation Services dominated the service segment, holding a 29.6% share, reflecting rising demand for timely and efficient delivery across global supply chains.

- 3PL/Contract Logistics accounted for a commanding 71.6% share in the logistics model segment, driven by integrated solutions that improve supply chain efficiency.

- Retail & E-commerce was the largest end-use sector with a 29.6% share, supported by rapid expansion of online shopping and fulfillment needs.

- Asia Pacific led globally with a 35.5% share in 2024, fueled by industrialization, growth in e-commerce, and digital transformation across China and India.

(source: market.us)

Global Economy & Geopolitics

The logistics industry in 2025 is being significantly shaped by the global economic and geopolitical landscape. Slower global economic growth, estimated at around 3.0% GDP increase for the year, and pronounced regional differences are creating a complex environment for logistics firms.

The United States shows relatively stable growth near 2.0%, driven by strong domestic demand even amid high interest rates. In contrast, Europe struggles with sluggish growth close to 1.2%, impacted by high energy costs and political instability.

China, facing external trade pressures and internal adjustments, expects a moderate recovery of roughly 4.5%. Emerging markets such as Southeast Asia, India, and Mexico are capitalizing on supply chain diversification, attracting investment and becoming vital players in global logistics networks. This uneven economic landscape demands adaptive strategies from logistics providers to manage shifting regional demand and risk.

Macroeconomic Indicators Review

The logistics industry must consider factors such as inflation, labor market conditions, and trade volumes. Unemployment rates remain elevated, for example, around 8.5% as of early 2025, which affects operational capacity and labor availability across regions. Export growth is weak, with goods exports showing minor gains of about +1.7% year-on-year early in the year, while services exports have declined by 4.0% in the first two quarters.

Freight markets are also adjusting from pandemic peaks to more normalized volumes, with ocean and air freight rates softening but not fully returning to pre-pandemic levels due to structural cost pressures. Capital markets show some confidence in prime logistics assets, with stable yields around 5.4% in major hubs.

US-China Trade War Impact

The US-China trade war remains the epicenter of disruption in global logistics. In 2025, tariff escalations have continued aggressively, with the US imposing tariffs as high as 145% on selected Chinese goods and China retaliating with tariffs up to 125% on American exports. These tariffs have reshaped trade flows, causing importers to rush shipments ahead of tariff deadlines, leading to artificial volume spikes followed by steep declines.

Particularly impactful is the removal of the US “de minimis” rule for low-value imports, which until August 29, 2025 allowed shipments below $800 to avoid duties. This policy change disrupts the direct-to-consumer e-commerce model reliant on Chinese goods and alters air cargo economics significantly.

The unpredictability of tariff extensions and pauses encourages logistics managers to balance freight cost optimization with political risk management, making geopolitical intelligence an essential capability. This shifting landscape demands flexible supply chains ready to adapt to new routes, regulations, and cost structures.

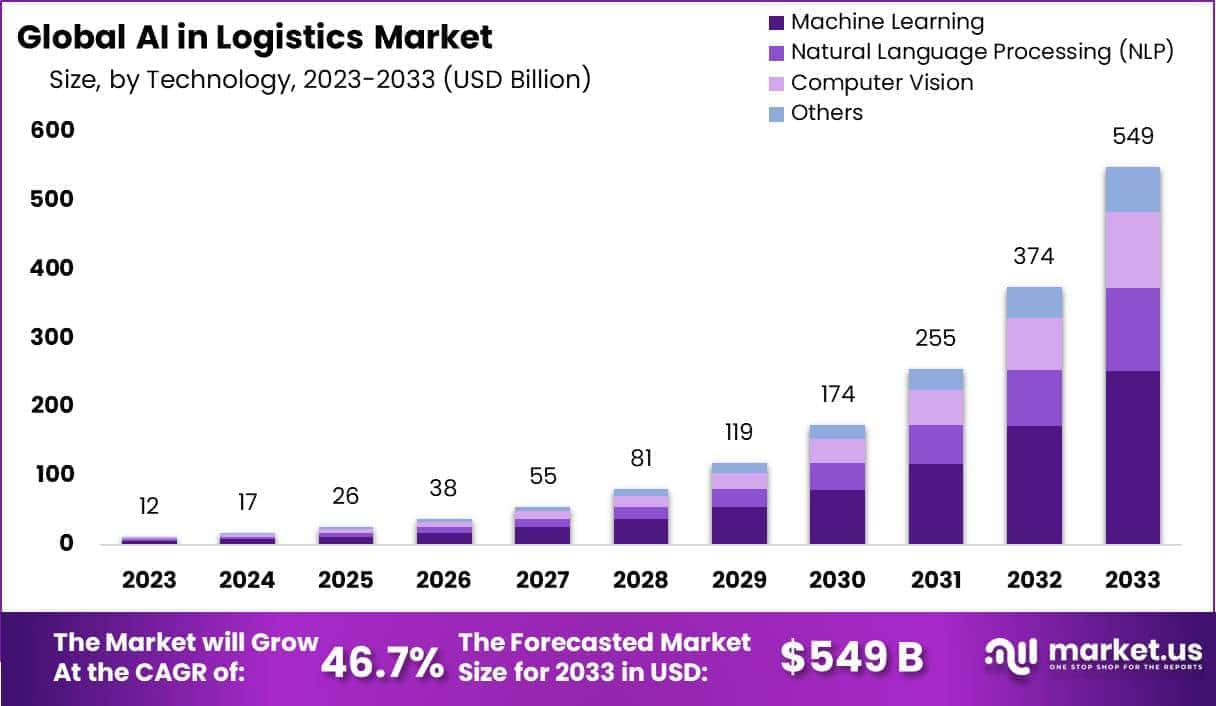

AI in Logistics Statistics

- The global market is projected to reach USD 549 billion by 2033, growing at an impressive CAGR of 46.7% (2024–2033).

- Machine Learning dominated the technology segment in 2023 with 46% share, reflecting its importance in optimizing logistics and supply chain operations.

- Inventory Control & Planning led the application segment, holding 32% share, underlining the significance of AI in efficient stock and resource management.

- The Retail sector accounted for over 29% share in 2023, showcasing rapid AI adoption to improve operations and enhance customer experience.

- North America led globally with 41% share, driven by strong U.S. adoption and advanced AI-driven logistics technologies.

- Predictive maintenance and asset monitoring adoption is growing by 45% (2022–2024), enabling early fault detection and prevention.

- About 50% of logistics firms are preparing for AI-powered autonomous warehouses by 2024, with robots handling picking and sorting.

- Over 65% of AI tools are expected to integrate with IoT devices by 2024, ensuring real-time communication and efficiency.

- AI-enabled last-mile delivery optimization is increasing by 40% between 2022 and 2024, enhancing speed and reliability.

- By 2024, 55% of logistics AI will leverage NLP and chatbots for smarter, customer-friendly interactions.

- Around 45% of logistics firms plan to deploy AI for supply chain risk management, improving resilience.

- Cybersecurity is a top priority, with 70% of AI platforms expected to feature advanced data protection by 2024.

- Freight matching and load optimization using AI is projected to increase by 35% between 2022 and 2024.

- By 2024, over 60% of AI in logistics will be deployed via cloud platforms, supporting scalability and flexibility.

(source: market.us)

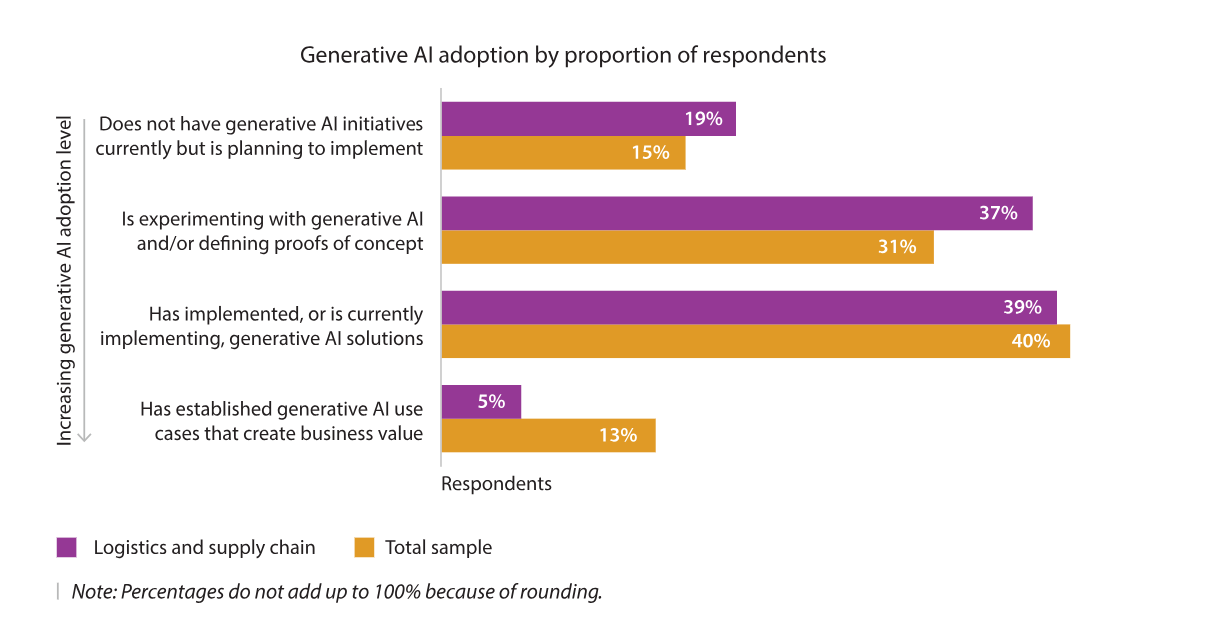

Cautious AI Adoption in Logistics

- 39% of logistics and supply chain respondents have implemented or are currently implementing generative AI solutions.

- 40% of the total sample have reached the same stage of generative AI implementation, showing similar adoption momentum.

- Only 5% of logistics companies have established AI use cases that deliver measurable business value.

- In contrast, 13% of the total sample have successfully created business value from generative AI.

- 37% of logistics respondents are still experimenting with AI or working on proof-of-concept projects.

- This is higher than the 31% reported across the total sample, indicating a slower path to maturity in logistics.

- 19% of logistics companies have no current AI initiatives but plan to implement them soon.

- This is slightly above the total sample’s 15%, reflecting a cautious but growing interest in AI adoption.

(source: infosys.com)

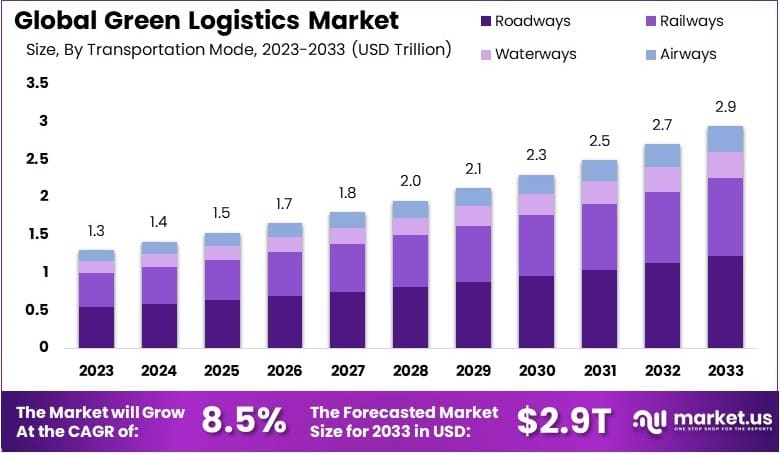

Green Logistics Statistics

- The market was valued at USD 1.3 trillion in 2023 and is projected to reach USD 2.9 trillion by 2033, growing at a CAGR of 8.5%.

- Roadways dominated the transportation mode segment with a 41.6% share, supported by the need for sustainable road transport.

- Solutions led the component segment with a 62.3% share, driven by demand for efficient and technology-enabled logistics management.

- Manufacturing emerged as the top industry vertical, reflecting increased adoption of green supply chain practices.

- Distribution dominated the business type segment, supported by rising demand for eco-friendly distribution networks.

- Europe held a 36.3% share of the market, valued at USD 0.47 trillion, driven by strict environmental regulations and sustainability mandates.

(source: market.us)

Key Investment Insights

- Tiger Global Management leads all investors with a substantial USD 4.1 billion invested across 56 companies, signaling strong conviction in logistics as a scalable and fast-evolving industry.

- Warburg Pincus has committed USD 2.9 billion to 24 companies, indicating a targeted approach toward long-term value creation in logistics infrastructure and services.

- Alibaba Group has invested USD 2.7 billion in 18 companies, reinforcing its strategic alignment of logistics with its broader e-commerce ecosystem.

- SoftBank Vision Fund has deployed USD 2.4 billion across 22 companies, focusing on disruptive and automation-led logistics solutions.

- DST Global invested USD 1.6 billion in 11 companies, with an emphasis on high-growth, tech-enabled logistics startups.

- Hillhouse Capital allocated USD 1.5 billion to 13 companies, targeting operational innovation and digital transformation in the supply chain.

- Sequoia Capital has injected USD 1.4 billion into 27 companies, backing next-generation logistics technologies aimed at improving speed, efficiency, and scalability.

Key Emerging Trends

- Digitization and automation, including AI, IoT, and process automation, are becoming fundamental to logistics operations.

- Trade flows are reconfiguring toward regionalization and nearshoring for shorter, more resilient supply chains.

- Customer expectations are rising with demands for faster delivery and better traceability.

- Continuous disruptions like pandemics, geopolitical conflicts, and extreme weather highlight the need for supply chain resilience.

- Environmental regulations and ESG pressures are driving companies to reduce their carbon footprint and increase transparency.

- Automation and robotics in warehouses, including collaborative robots (cobots), improve efficiency and accuracy.

- Digital twins and IoT sensors enable real-time visibility and better decision-making across logistics processes.

- The last mile is being transformed by microhubs, smart lockers, AI-driven routing, and testing of drones and autonomous vehicles.

- Nearshoring strategies are gaining traction to reduce risks, transit times, and respond locally to demand.

- 5G connectivity supports real-time fleet monitoring, logistics automation, and integration of cloud-based systems.

Technology and Innovation

Technology is the central driver of change in logistics. Increasingly, companies are adopting:

- Automation and robotics: Smart warehouses use collaborative robots (cobots) to handle repetitive tasks, reducing errors and speeding operations. Automated sorting, cross-docking, and real-time inventory management are becoming common.

- Digital twins and IoT: Digital twins allow simulation and optimization of logistics processes before implementation, reducing risks. IoT sensors track shipments in real-time for location, temperature, and condition, critical for sensitive goods like pharmaceuticals.

- Artificial Intelligence (AI): AI optimizes inventory planning, transport routing, and demand forecasting. AI implementation is reported to reduce logistics costs by up to 15%, inventory levels by 35%, and improve service by 65% for early adopters.

- Predictive analytics: Real-time data from vehicles and machinery helps detect anomalies and optimize routes and warehouse locations.

- Drone deliveries: Trials in certain regions aim for faster, cost-effective last-mile delivery with drones expected to become a significant segment in the near future.

- Blockchain: Emerging as a tool to improve transparency and security across the supply chain by providing tamper-proof transaction records.

Challenges and Opportunities

The logistics sector faces several challenges but also opportunities for growth:

- Digital integration: Many companies still struggle to integrate new technologies due to legacy systems and high investment requirements. There is a need to balance cost with the benefits of digital transformation.

- Labor shortages: Skilled labor scarcity drives adoption of automation and robotics, but companies must also manage the transition and workforce training.

- Sustainability pressures: Meeting environmental regulations and ESG criteria requires investment in greener fleets, renewable energy, and efficient practices but builds long-term value and consumer trust.

- Supply chain resilience: Geopolitical risks, pandemics, and climate events force companies to redesign supply lines to be more regional and agile, which offers competitive advantage but requires re-planning and capital expenditure.

- Customer experience: The surge in e-commerce demands faster deliveries and full shipment transparency, pushing logistics providers to innovate in last-mile delivery and real-time tracking.

Conclusion

The logistics industry is entering a phase of accelerated transformation, driven by globalization, digitalization, and evolving trade policies. With robust growth projections and an expanding role of advanced technologies, the sector is adapting to increasing demands for speed, efficiency, and sustainability.

Emerging opportunities in autonomous trucking, waterway transport, and rail logistics are expected to reshape cost structures and strengthen supply chain resilience. Meanwhile, regional shifts, such as the anticipated dominance of North America from 2025 onward, highlight the influence of e-commerce and last-mile delivery innovations on global logistics competitiveness.

For businesses and professionals in logistics and supply chain management, understanding these statistics and market trends is essential. The ability to adapt to digital tools, navigate trade agreements, and optimize multimodal transport strategies will determine long-term success in the evolving landscape of global trade and transportation.

References

- https://www.infosys.com/iki/research/logistics-industry-outlook-2025.html

- https://gitnux.org/logistic-industry-statistics/

- https://tech.co/logistics/logistics-statistics-numbers-to-know

- https://cashflowinventory.com/blog/logistics-statistics/

- https://www.startus-insights.com/innovators-guide/logistics-report-2024/

- https://www.clickpost.ai/blog/logistics-statistics-and-insights

- https://www.pispl.in/logistics-technology-trends-to-watch-out-for-in-2025.php

- https://acrosslogistics.com/blog/en/logistics-trends

- https://sjlogistics.co.in/blogs/top-10-logistics-trends-2025/

- https://www.linkedin.com/pulse/logistics-2025-innovations-challenges-opportunities-mfi4c/

- https://www.conquerornetwork.com/blog/2025/01/08/key-challenges-freight-forwarders-will-face-in-2025/

- https://www.cleo.com/blog/logistics-management-trends

- https://wifitalents.com/logistics-industry-statistics/

- https://www.tgl-group.net/en/search-detail1006_36_0.html

- https://www.wiima.com/global-logistics-market-update-navigating-the-post-peak-landscape-in-h2-2025/

- https://www.linkedin.com/pulse/navigating-storm-us-china-trade-war-its-impact-global-aboobaker–oufrc

- https://grydd.com/the-us-china-trade-war-ripple-effects-on-the-global-supply-chain/