Introduction

Semiconductor Statistics: A semiconductor is a material that sits in the middle between a conductor and an insulator. This means it can sometimes allow electricity to flow and other times block it, depending on how it is used. Semiconductors are mostly made of silicon and are used inside chips and electronic circuits. These materials are crucial because they let devices switch signals on and off, which is how computers, phones, and modern electronics function. Without semiconductors, most of today’s technology would not be possible.

At the semiconductor industry, we see an area experiencing impressive growth. In 2025, the market value is expected to reach around $602.2 billion, showing a year-over-year growth rate of 6.5% (by market.us). The main factors driving this growth include high demand for logic and memory chips, improvements in computing power, data centers, artificial intelligence, and smart electronics. Companies are actively investing in areas such as generative AI and edge computing.

This article provides a detailed and up-to-date analysis of the global market, including segmental shares and insights from 2025. It highlights the latest trends, growth patterns, and key factors shaping the industry. Let’s explore some important statistics to better understand its size, trajectory, and the impact it continues to have on the world.

Top Editor’s Choice

- Total semiconductor sales worldwide are expected to reach USD 588.36 billion in 2024.

- Industry revenue for 2024 is projected at USD 627 billion, marking 19% growth.

- Memory semiconductor sales are estimated at USD 129.8 billion in 2024, up 44.8% from 2023.

- Global semiconductor sales are forecast to hit USD 697 billion, on track toward USD 1 trillion by 2030.

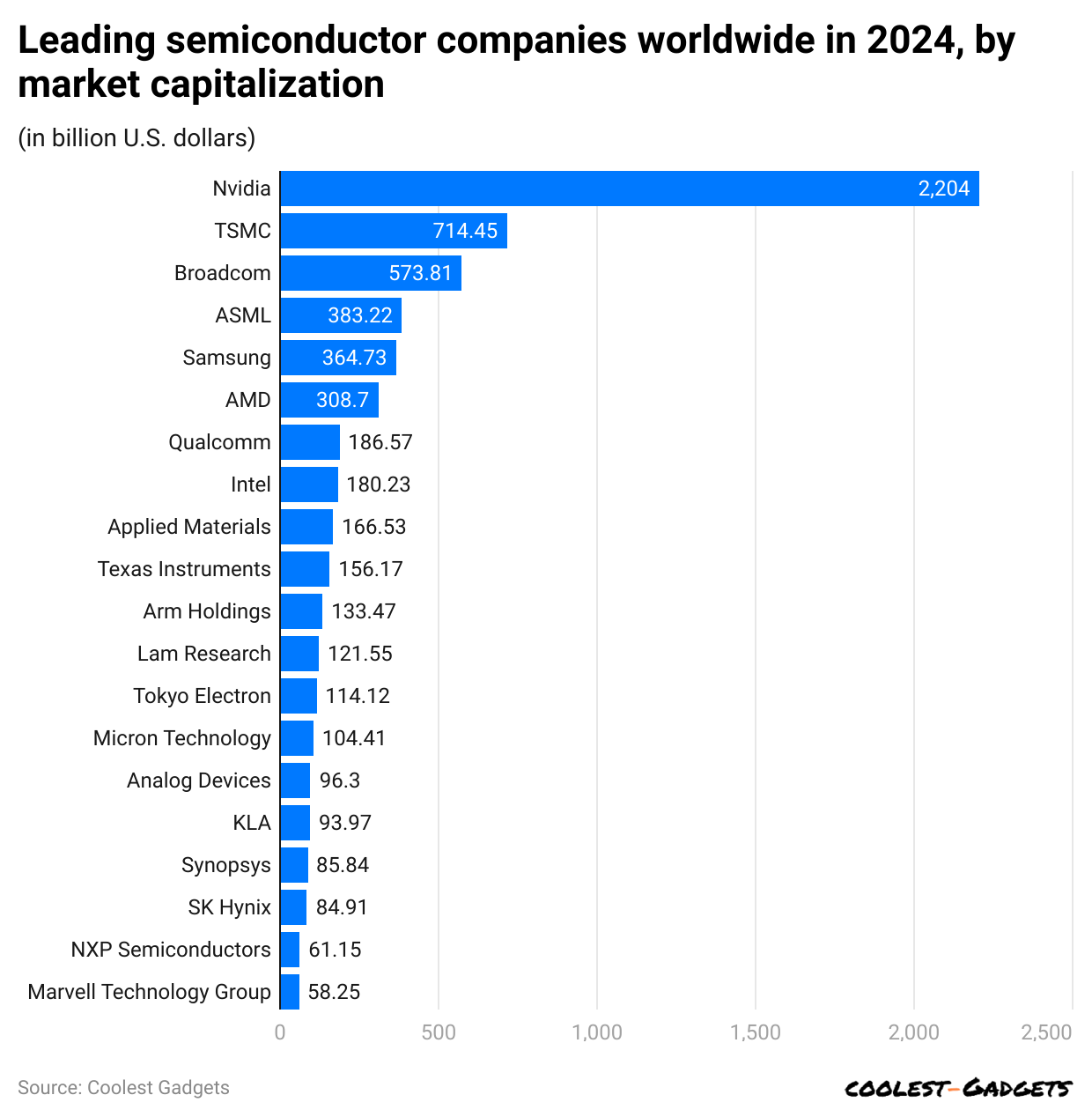

- Nvidia leads by market capitalization at USD 2,204 billion, followed by TSMC (USD 714.45 billion) and Broadcom (USD 573.81 billion).

- Capital expenditures in 2025 are expected to reach USD 185 billion, expanding capacity by 7%.

- Semiconductors support over 300 downstream industries, accounting for 26 million U.S. workers.

- The U.S. industry employs 300,000 directly and supports nearly 2 million indirect jobs.

- DRAM will make up 14% of semiconductor revenue in 2024.

- HBM is forecast to grow at 64% CAGR (bit growth) and 58% CAGR (revenue) through 2028.

- Industry profit margins rose from 23.5% to 28.6% in 2024, despite economic challenges.

- 1 billion edge AI chips in smartphones are expected to ship in 2024.

- Global capital spending is projected at USD 146.6 billion, down 19% YoY.

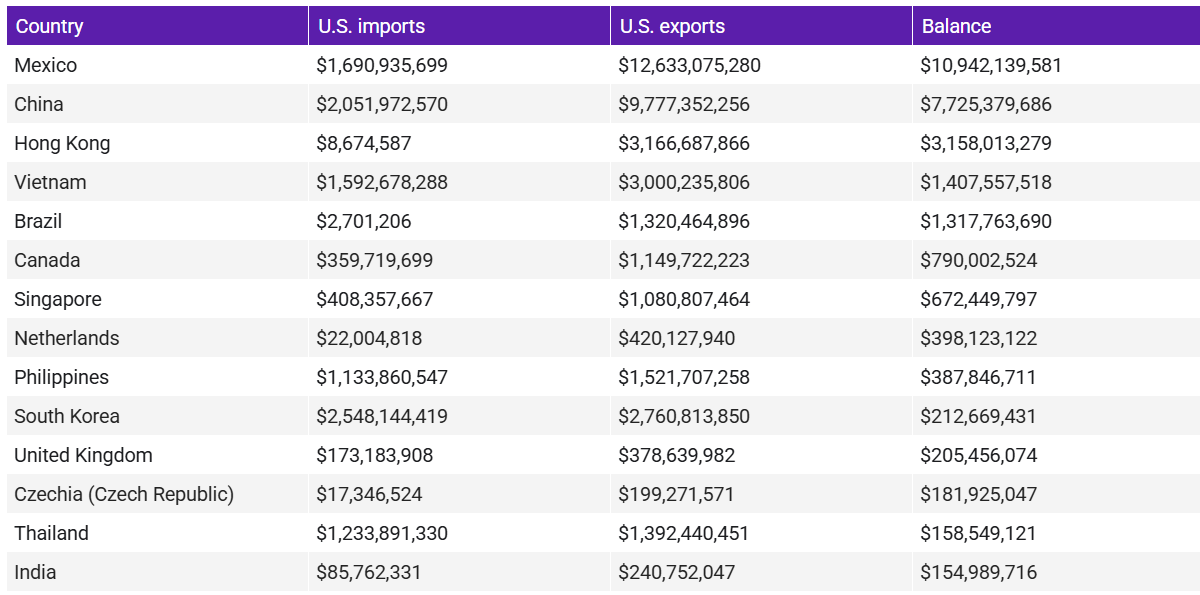

- In March 2023, the U.S. exported USD 125 million in semiconductors to Mexico and USD 60.1 million to Germany.

- The U.S. semiconductor workforce counts 338,000 professionals across design, manufacturing, and equipment.

U.S. semiconductor imports and exports

In 2024, the United States recorded a $11 billion trade surplus in semiconductors, reflecting its strong position in global chip manufacturing and design. The country maintained a positive semiconductor trade balance with 154 nations, while only 28 countries reflected a negative balance. This broad base of trade partners highlights the strategic advantage held by the U.S. in technology-intensive products that remain central to digital transformation, consumer electronics, automotive systems, and defense applications.

The historical trajectory of the U.S. trade balance in semiconductors shows a dynamic shift in competitiveness. In 2004, the surplus stood at $21 billion, but by 2016 it had eroded into a $2 billion deficit, underscoring pressures from rising global competition and supply chain dependencies. Since then, recovery efforts, strengthened by domestic production capabilities, R&D leadership, and supportive trade strategies, have turned the balance positive again.

(credit: fool.com)

Revenue Statistics

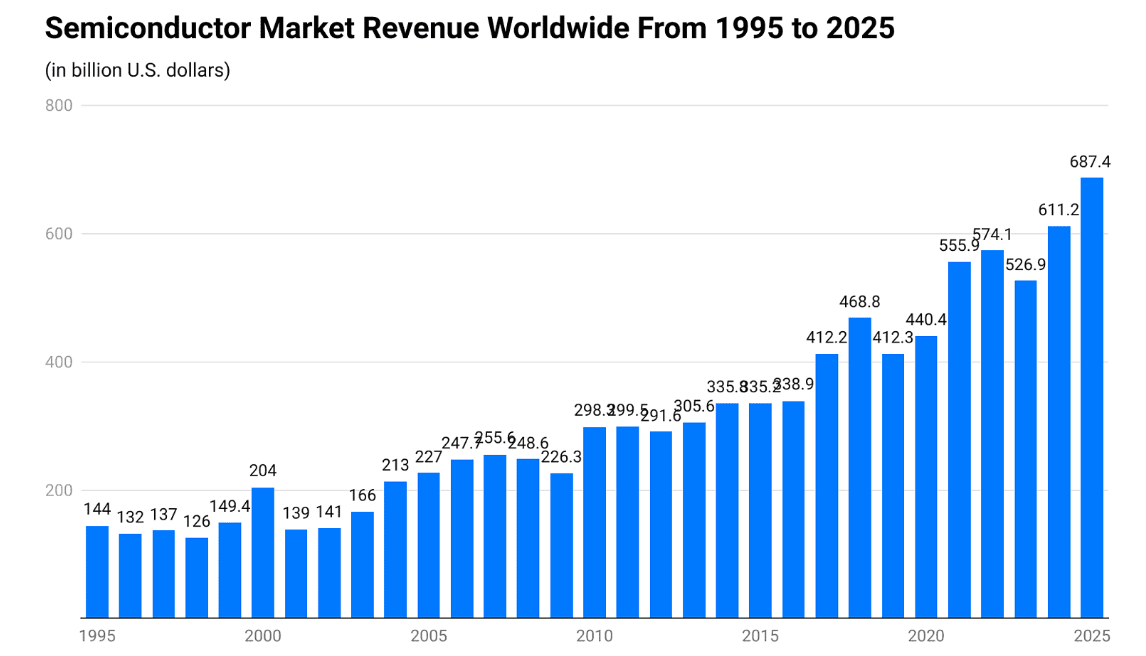

- The global semiconductor market expanded from $144 billion in 1995 to a projected $687.4 billion in 2025, showing its rise as a central pillar of the digital economy.

- Growth has not been linear, with downturns in 2001 (drop from $204 billion to $139 billion) and 2009 (fall from $255.6 billion to $226.3 billion) caused by economic slowdowns and cyclical demand shifts.

- Each downturn was followed by strong recovery, reflecting the resilience of the industry and its ability to adapt to global shocks and demand cycles.

- After 2017, growth accelerated sharply, with revenues moving from $338.9 billion in 2015 to $555.9 billion in 2021, supported by cloud computing, smartphones, and the rise of connected vehicles.

- Pandemic-driven demand for laptops, smartphones, and data centers boosted revenues, though supply chain shortages created new structural challenges.

- The projected $687.4 billion in 2025 highlights momentum driven by AI, 5G, edge computing, and autonomous mobility, making semiconductors indispensable for future innovations.

(credit: coolest-gadgets)

Financial Performance Statistics

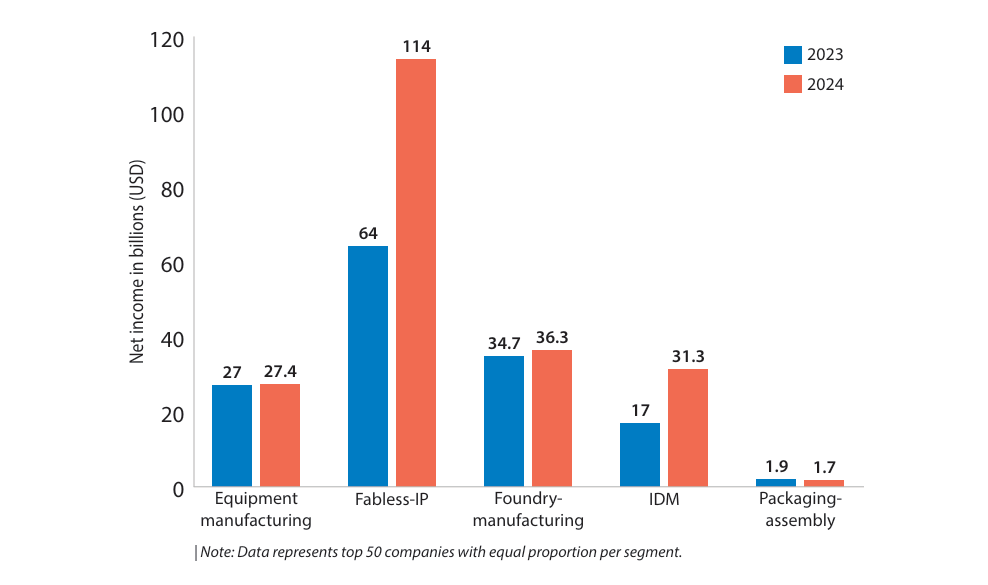

- In equipment manufacturing, net income remained almost flat, moving from $27 billion in 2023 to $27.4 billion in 2024, showing stability but limited growth in this segment.

- The fabless-IP segment recorded the strongest performance, rising from $64 billion in 2023 to $114 billion in 2024. This sharp increase highlights the strength of design-focused companies that rely on outsourcing production, benefiting from rising demand for advanced chips.

- Foundry manufacturing showed moderate growth, moving from $34.7 billion in 2023 to $36.3 billion in 2024, reflecting steady demand for contract manufacturing services as chipmakers expand capacity.

- The IDM (Integrated Device Manufacturer) segment almost doubled its net income, increasing from $17 billion in 2023 to $31.3 billion in 2024. This indicates that companies managing both design and production are regaining competitiveness, supported by vertical integration and technology leadership.

- The packaging and assembly segment declined slightly, from $1.9 billion in 2023 to $1.7 billion in 2024, reflecting margin pressures and the highly cost-sensitive nature of this part of the value chain.

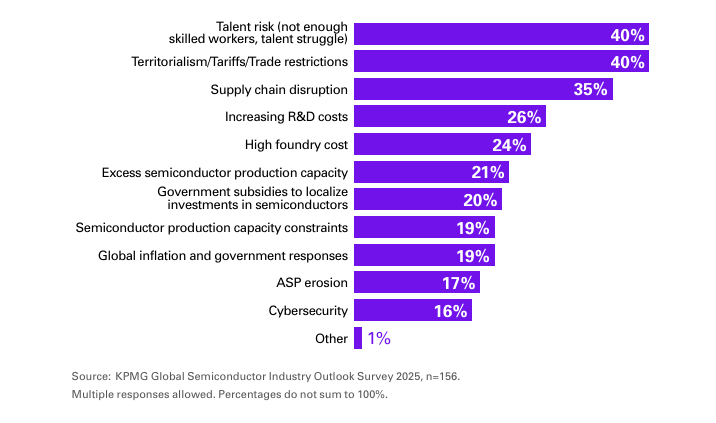

Industry Issues and Strategic Priorities

Territorialism, tariffs, and talent risk are identified as the two biggest issues for the semiconductor industry over the next three years. These risks highlight both geopolitical pressures and the challenge of retaining skilled professionals in an industry that requires deep expertise.

Supply chain flexibility and talent development/retention stand as the top strategic priorities for executives. Alongside these, digital transformation and the integration of generative AI (GenAI) are expected to shape the industry’s competitive direction.

The rise of nontraditional semiconductor companies, such as tech giants, platform providers, and automotive firms, is creating new competitive pressures. Executives are particularly concerned that these entrants will intensify the fight for scarce technical talent.

(credit: KPMG)

Financial Expectations

- On the financial side, 86% of executives project revenue growth in 2025, signaling strong confidence in market demand despite macroeconomic and geopolitical challenges.

- 63% of companies expect to increase capital spending on semiconductor infrastructure, reflecting ongoing commitments to expand capacity and strengthen manufacturing resilience.

- 72% of leaders predict higher R&D spending, underlining the importance of continuous innovation in chip design, advanced materials, and new architectures to secure future competitiveness.

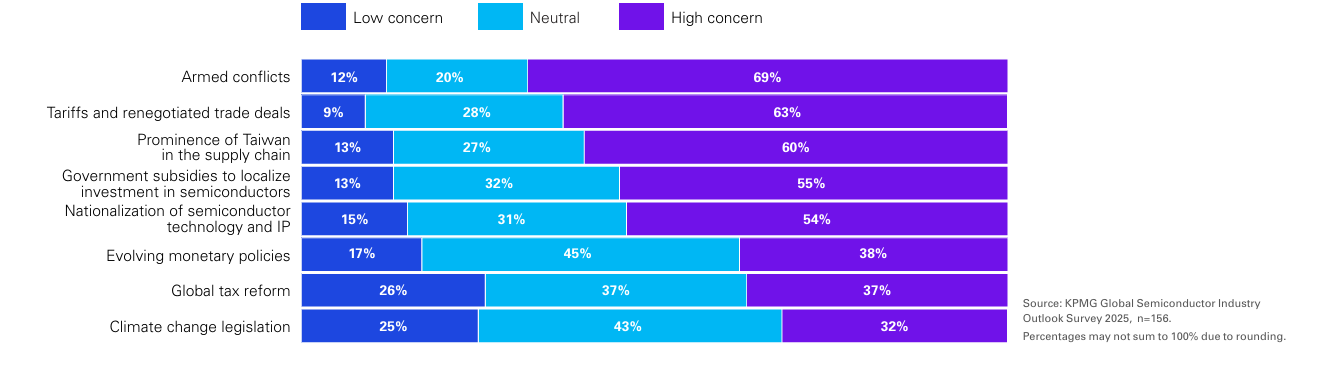

Geopolitical Impact

The survey highlights that armed conflicts are the top geopolitical concern, with 69% of respondents expressing high concern, while only 12% reported low concern. This underscores the sector’s vulnerability to global instability and its potential to disrupt supply chains and trade flows.

tariffs and renegotiated trade deals are the second most pressing issue, with 63% of executives highly concerned. The industry is acutely aware that new trade barriers or renegotiations could significantly affect semiconductor flows across borders, impacting both costs and supply reliability.

The prominence of Taiwan in the supply chain is also a major focus, with 60% citing high concern. Given Taiwan’s central role in advanced chip manufacturing, any disruption creates substantial global risk, explaining the heightened sensitivity from industry leaders.

Concerns around government subsidies for semiconductor localization and the nationalization of semiconductor technology and IP are also high, at 55% and 54% respectively. These issues highlight fears of market fragmentation and the potential for uneven competitive landscapes as countries push for greater self-sufficiency.

In comparison, evolving monetary policies, global tax reform, and climate change legislation rank lower on the list of immediate threats. Only 38% expressed high concern for monetary policies, while both global tax reform and climate change legislation split concerns equally between neutral and high levels, around 37% and 32% respectively.

(credit: KPMG)

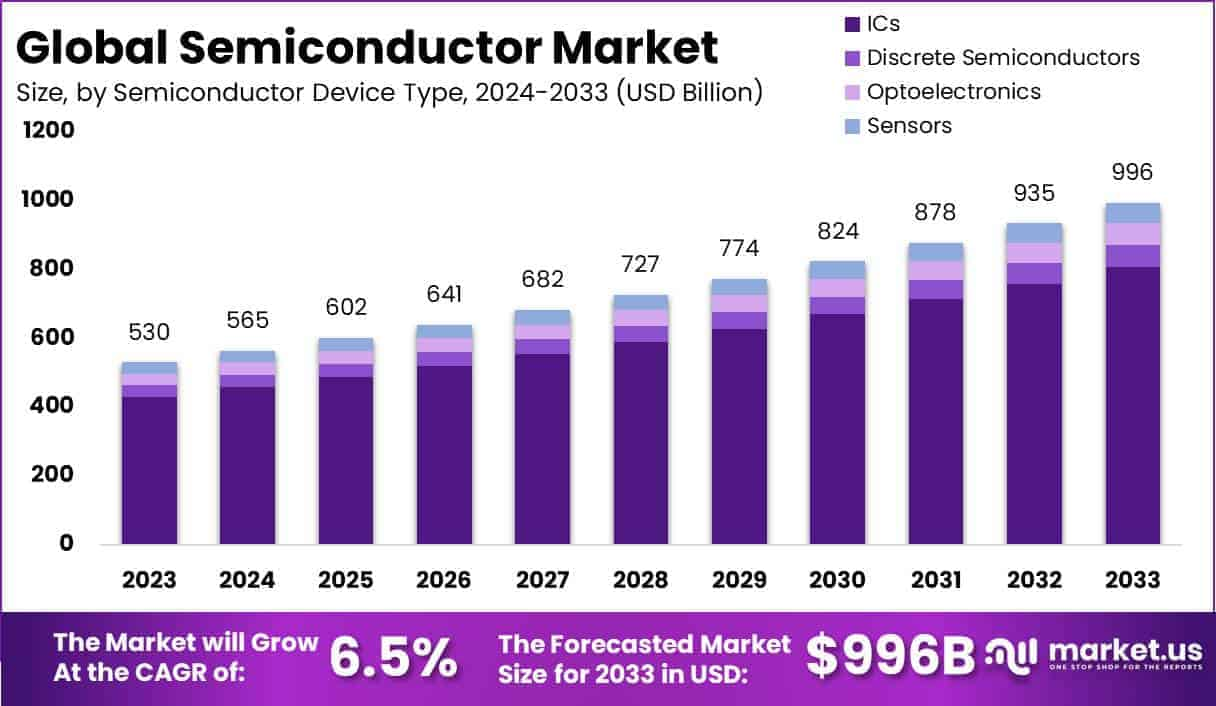

Semiconductor Market Size

- The Global Semiconductor Market is projected to touch nearly USD 996 Billion by 2033, growing steadily at a 6.5% CAGR from 2024 to 2033. This reflects the long-term strength of semiconductor demand across multiple industries.

- In 2023, the Integrated Circuits (ICs) segment dominated with over 81.3% share, confirming its central role in powering computing, communications, and automotive technologies.

- The Consumer Electronics segment, covering mobile and computing devices, captured more than 61% of the market in 2023, highlighting how everyday devices remain the largest demand driver for semiconductors.

- Asia-Pacific accounted for 63.91% of the global semiconductor market, establishing itself as the primary growth engine, supported by manufacturing hubs, government initiatives, and strong consumption in China, South Korea, and Taiwan.

(credit: market.us)

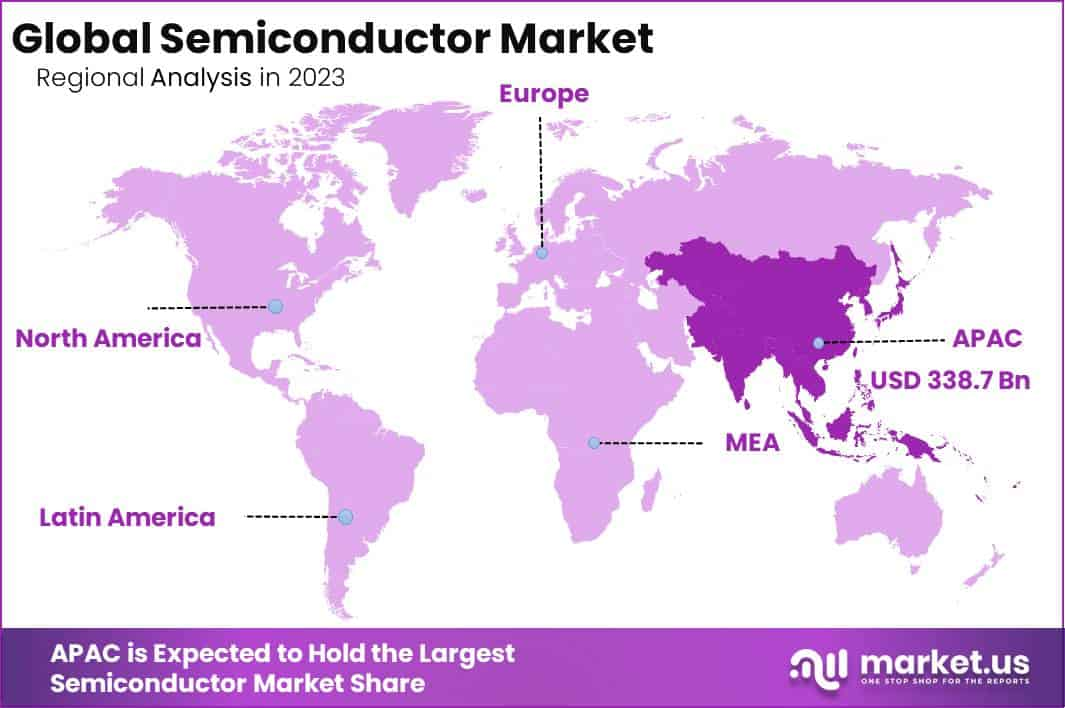

Semiconductor Market Statistics by Region

In 2023, Asia-Pacific (APAC) accounted for 63.91% of the global semiconductor market, generating revenues of USD 388.7 billion. This dominant position reflects the region’s strong manufacturing ecosystem, supported by extensive fabrication capacity and technological expertise. Countries such as Taiwan, South Korea, and China serve as the core hubs, hosting the world’s leading foundries and memory chip producers, which continue to anchor the region’s leadership.

(credit: market.us)

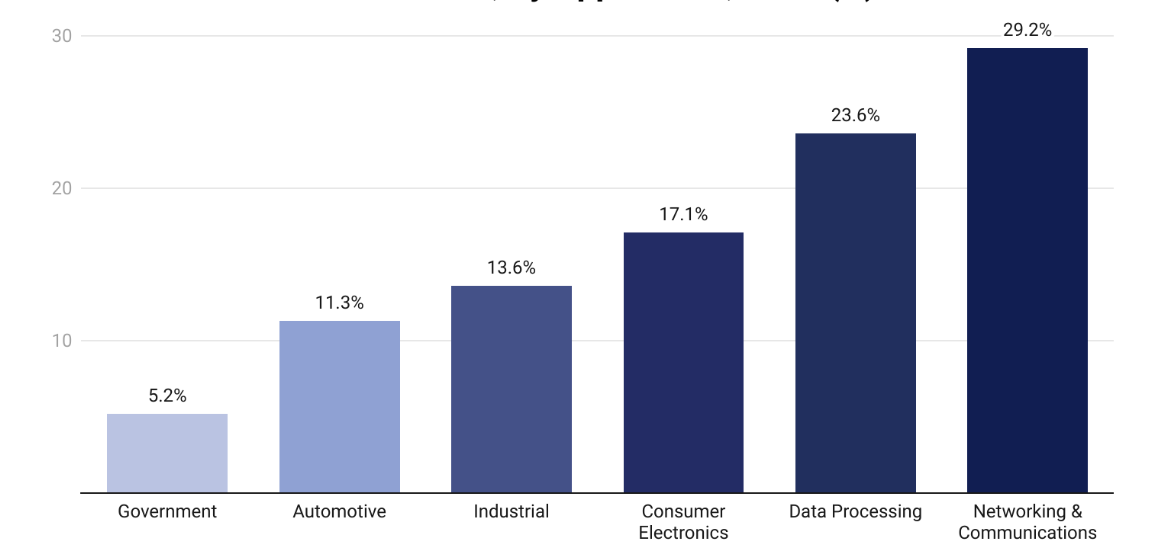

By Application Analysis

- The Network and Communication segment led the semiconductor industry in 2023, accounting for the highest revenue share of 29.2%, reflecting the strong demand for 5G infrastructure, cloud connectivity, and advanced networking solutions.

- The Data Processing segment contributed 6%, while Consumer Electronics generated a solid 17.1% share, driven largely by mobile devices, laptops, and personal computing equipment.

- Among other applications, Industrial use accounted for 13.6%, supported by automation and smart manufacturing adoption.

- The Automotive sector held 11.3%, underscoring the rising role of semiconductors in electric vehicles, driver-assistance systems, and connected mobility solutions.

- The Government segment contributed 5.2%, reflecting investments in defense, aerospace, and public infrastructure relying on advanced semiconductor technologies.

(Reference: precedenceresearch.com, coolest-gadgets.com)

Market Capitalization of Leading Semiconductor Companies

Types of Semiconductor Industry’s Revenue Statistics

| Type | 2023 Revenue (USD Bn) | 2024 Revenue (USD Bn) | Growth (2024 vs 2023) |

|---|---|---|---|

| Memory Semiconductors | 89.6 | 129.8 | 44.8% |

| Logic Semiconductors | 174.9 | 191.7 | 9.6% |

| Analog Semiconductors | 81.05 | 84.06 | 3.7% |

| Micro Semiconductors | 76.68 | 81.94 | 7.0% |

| Optical Semiconductors | 42.58 | 43.32 | 1.7% |

| Discrete Semiconductors | 33.95 | 37.46 | 4.2% |

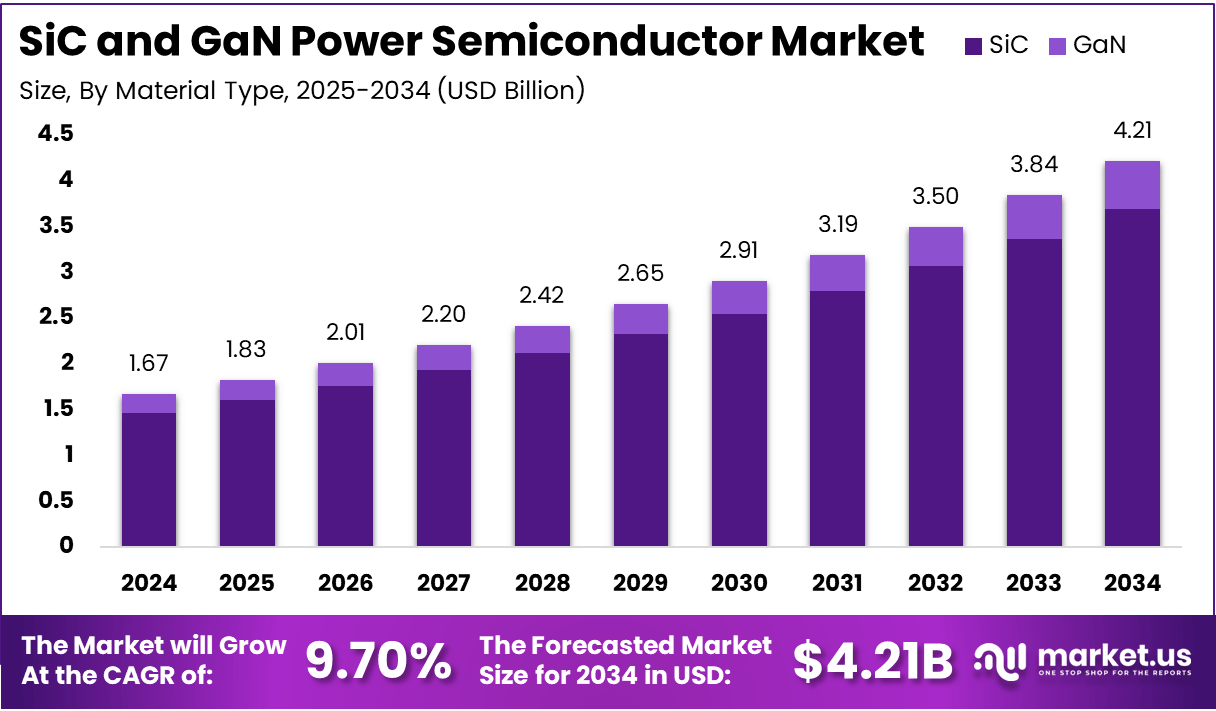

SiC and GaN Power Semiconductor Market Statistics

- The global market was valued at USD 1.67 billion in 2024 and is expected to reach USD 42.1 billion by 2034, growing at a robust 9.70% CAGR, supported by the accelerating shift toward electrification and energy efficiency.

- By material type, SiC captured 87.7% of the market, underscoring its critical role in high-performance and high-voltage applications where efficiency and durability are essential.

- In terms of power range, the high-power segment accounted for 75.9%, reflecting strong usage in sectors such as renewable energy, industrial power equipment, and electric mobility.

- By application, the automotive sector dominated with 73.4%, fueled by rapid adoption of electric vehicles (EVs), charging infrastructure, and advanced driver-assistance systems (ADAS).

- Geographically, Asia Pacific led with 52.8% share, driven by its strong manufacturing base, supportive government policies, and rising demand from automotive and industrial markets.

(credit: market.us)

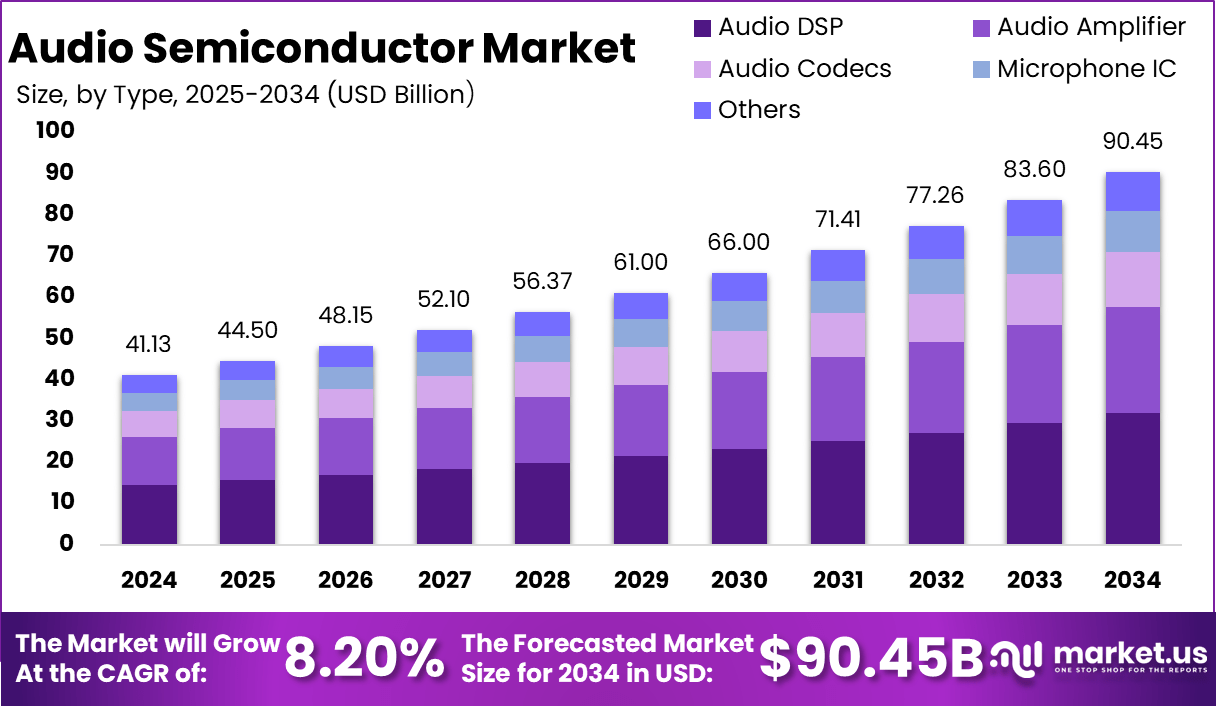

Audio Semiconductor Market Statistics

- The market is expected to expand from USD 41.13 billion in 2024 to USD 90.45 billion by 2034, supported by a steady 8.20% CAGR, reflecting strong demand for advanced audio technologies.

- By type, Audio DSPs hold 41.4% share, confirming their dominance in enabling sound processing, noise cancellation, and immersive audio features across devices.

- By application, smartphones lead with 39.6%, showcasing how mobile devices remain the largest consumer of audio semiconductors as users demand premium audio quality.

- Regionally, Asia Pacific contributes 51.3%, highlighting its strong role in electronics manufacturing and consumer demand for audio-enabled devices.

- The market shows substantial growth potential, driven by high consumer expectations for sound quality in smartphones, smart home devices, wearables, and automotive systems, supported further by innovations such as AI-powered audio enhancement and 3D audio processing.

(credit: market.us)

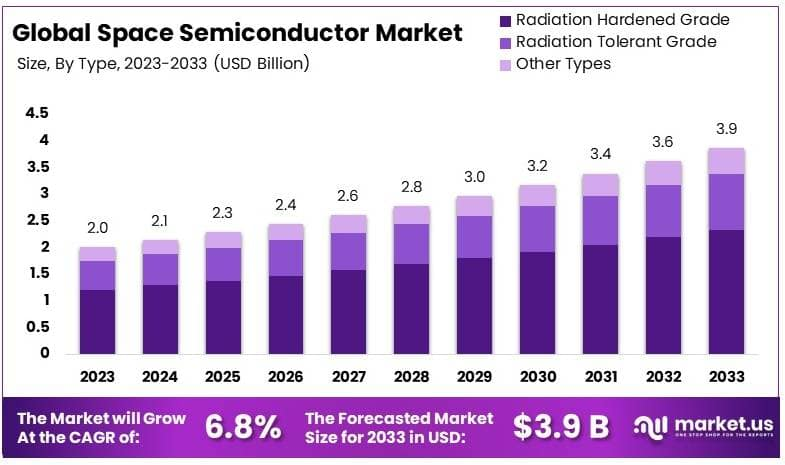

Space Semiconductor Market Statistics

- The market was valued at USD 2.0 billion in 2023 and is projected to reach USD 3.9 billion by 2033, growing at a steady 6.8% CAGR, supported by increasing demand for advanced electronic systems in space programs.

- By type, Radiation Hardened Grade accounted for 60.5%, underscoring its importance in withstanding extreme radiation and temperature variations in space environments.

- By component, Integrated Circuits led with 26.1%, highlighting their essential role in powering communications, navigation, and mission-critical systems in spacecraft.

- By application, the Satellite segment dominated with 56.8%, reflecting the growing reliance on satellites for communication, defense, navigation, and Earth observation.

- Regionally, North America captured 42.0%, driven by strong government investments, defense programs, and the presence of major space technology companies supporting exploration and satellite expansion.

(credit: market.us)

Compound Semiconductor Market Statistics

- The market is projected to rise from USD 39.4 billion in 2023 to USD 94.8 billion by 2033, growing at a strong 9.2% CAGR, supported by rising demand for high-performance materials in electronics and communication.

- By type, Gallium Nitride (GaN) led with over 28% share in 2023, reflecting its wide use in high-frequency, high-power, and energy-efficient applications.

- By product, LEDs dominated with more than 35% share, showcasing their central role in lighting, displays, and automotive technologies.

- By application, IT and Telecom held over 40% share, underlining the reliance of next-generation communication systems on compound semiconductors for speed and efficiency.

- Regionally, Asia Pacific led with 55% share, generating USD 21.68 billion in 2023, supported by its strong semiconductor manufacturing ecosystem and growing adoption across consumer electronics and telecom sectors.

(credit: market.us)

The Future of Semiconductors

The future of semiconductors is unfolding at a remarkable pace. Market experts forecast that in 2025, the industry will continue its upward trajectory, driven mostly by the soaring demand for artificial intelligence, data centers, and next-generation electronics. Global sales are expected to expand by over 11% year-over-year, reaching a value of around $700.9 billion.

Countries and companies are pouring significant investments into expanding capacity and innovation, including more than half-a-trillion dollars in new manufacturing projects within the United States. The industry is preparing for a new era defined by smarter, faster, and more energy-efficient chips that can power everything from cloud computing to autonomous vehicles.

Recent developments

Recent developments have further confirmed this momentum. In 2025, landmark announcements include India’s successful production of its first indigenous semiconductor chip, marking a milestone in the country’s bid to strengthen its tech ecosystem.

The Union Cabinet in India also greenlit the establishment of another semiconductor plant as part of the national mission, showing how governments are helping reshape the global supply chain landscape. At the same time, major global players are bringing advanced packaging, 3D stacking, and new materials like silicon carbide and gallium nitride into mainstream chip manufacturing.

AI-driven design automation and the use of digital twins are making the entire manufacturing process more efficient, improving both speed and performance. These advancements are also ensuring better yields, reduced waste, and faster turnaround from lab to market.

Conclusion

In conclusion, the semiconductor industry stands on a foundation of robust growth, innovation, and geopolitical significance. Rising interest in custom chip development, combined with the ever-increasing computing needs of AI and cloud services, is transforming how chips are designed, manufactured, and deployed.

Although challenges remain – such as supply chain vulnerabilities and the need for skilled talent – the sector is more agile and resilient than ever. Its future will be shaped by ongoing investment, close collaboration between industry and government, and the relentless push toward more powerful, efficient, and sustainable technology.

Sources:

- https://www.deloitte.com/us/en/insights/industry/technology/technology-media-telecom-outlooks/semiconductor-industry-outlook.html

- https://www.fool.com/research/semiconductor-trade-statistics-tariffs

- https://coolest-gadgets.com/semiconductor-industry-statistics/

- https://kpmg.com/kpmg-us/content/dam/kpmg/pdf/2025/global-semiconductor-industry-outlook-2025.pdf

- https://www.pwc.com/gx/en/industries/technology/state-of-the-semicon-industry.html